The mood in crypto markets has shifted from cautious optimism to something closer to dread. Bitcoin’s price has slid sharply, volatility has returned, and the familiar metric known as the “Fear and Greed Index” has plunged into what analysts label “extreme fear.” For veterans of the space, this emotional whiplash is nothing new. For newer participants, however, the question feels urgent and personal: how low can this go, and what happens next?

Bitcoin’s recent downturn has been driven by a convergence of factors rather than a single catalyst. Macro uncertainty remains dominant, with global markets digesting persistent inflation concerns, shifting interest rate expectations, and renewed questions about economic growth. Risk assets across the board have felt pressure, and crypto has once again behaved less like a safe haven and more like a high-beta speculative asset. When liquidity tightens and confidence wobbles, Bitcoin is often among the first to feel it.

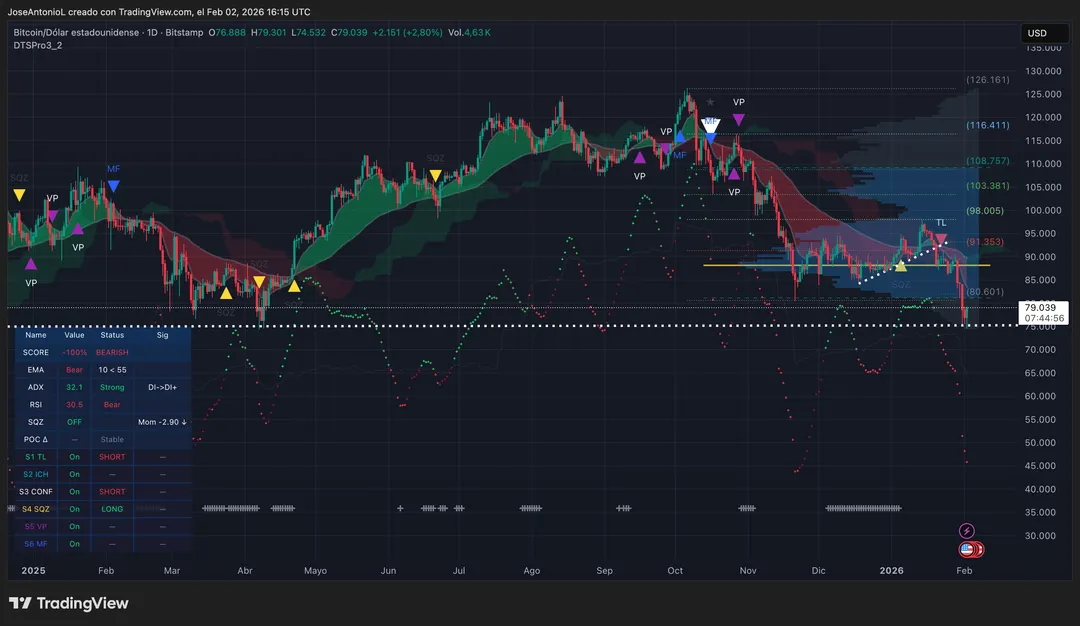

The Fear and Greed Index, which aggregates volatility, momentum, trading volume, and sentiment indicators, has become a psychological barometer for the market. When it flashes “extreme fear,” it signals widespread pessimism and risk aversion.

Historically, those moments have coincided with panic selling, forced liquidations, and emotionally driven decisions rather than sober long-term analysis. That does not guarantee an imminent bottom, but it does suggest the market is being ruled by anxiety rather than euphoria.

Price history offers both caution and perspective. Bitcoin has repeatedly suffered drawdowns of 50 percent or more during past cycles, including within broader bull markets. Each time, narratives emerged declaring the experiment finished, the technology broken, or adoption permanently stalled. Each time, Bitcoin eventually stabilized, rebuilt, and reached new highs. That pattern does not promise repetition, but it does undermine claims that fear alone signals terminal decline.

Some analysts point to technical levels that could come into play if selling accelerates. These projections are not prophecies but educated guesses based on prior support zones, moving averages, and on-chain data. What they share is an acknowledgment that markets rarely move in straight lines. Sharp drops often overshoot rational valuation as leverage unwinds and weaker hands exit, creating conditions that look irrational in hindsight.

Beyond charts, there is a deeper debate playing out about Bitcoin’s role in a changing financial system. Supporters argue that long-term adoption trends remain intact: institutional infrastructure continues to develop, sovereign debt levels remain historically high, and trust in centralized financial management is fragile.

Critics counter that Bitcoin is still too dependent on speculative capital and too correlated with traditional risk assets to fulfill its original promise as an alternative monetary system. Both arguments carry weight, and neither is resolved by short-term price action.

There is also a quieter conversation happening among long-time observers who are skeptical of purely organic explanations. While there is no definitive proof of coordinated suppression or manipulation at scale, it is documented that large players, derivatives markets, and leverage dynamics can amplify moves far beyond what spot demand alone would produce. This is not evidence of a grand conspiracy, but it is a reminder that markets are shaped by power, incentives, and structure as much as by ideology or belief.

What tends to be forgotten in moments of extreme fear is that markets are cyclical not just in price, but in psychology. Fear drives selling, selling creates discounts, and discounts eventually attract buyers with longer time horizons. That process can take weeks or months, and it can feel unbearable while it unfolds. Yet it is precisely in these moments that the difference between conviction and speculation is tested.

Bitcoin’s future will not be decided by a single dip, index reading, or headline. It will be shaped by how it performs across cycles, crises, and changing political and economic realities. Extreme fear may still give way to further downside, but it has also historically marked periods when the loudest voices were the most wrong. Whether this moment becomes another footnote or a turning point will only be clear in retrospect, but the panic itself is already telling a familiar story.

{kind=link}