(The Economic Collapse Blog)—The alarms are getting even louder each week. It has become exceedingly clear that the U.S. economy has entered a crisis that is similar to what we experienced in 2008 and 2009, and a lot of people are really starting to freak out. For those that cannot see the stunning parallels between the Great Recession and what we are going through now, I don’t know what to say to them. There are a lot of people out there that simply choose to believe whatever they want to believe no matter what the evidence indicates. In this case, all of the evidence is pointing in a single direction.

When foreclosure filings started to spike prior to the global financial crisis in 2008, that was a major red flag.

Now it is happening again.

In fact, during the month of October 2025 foreclosure filings were 19 percent higher than they were in October 2024…

In October alone, there were 36,766 foreclosure filings — the first step in the process, when a lender warns a borrower they’re in default. That’s up three percent from September and 19 percent from a year ago.

‘Foreclosure activity continued its steady upward trend in October — the eighth straight month of year-over-year increases,’ said ATTOM CEO Rob Barber.

The rise is stirring uncomfortable memories of 2008, when a wave of foreclosures triggered the worst housing crash in modern US history.

Read the second paragraph in that quote again.

Foreclosure activity has increased for eight consecutive months.

That is what we call a trend.

Some of the markets that were once the hottest are now seeing the highest rates of foreclosure filings…

States with the worst foreclosure rates were Florida (one in every 1,829 housing units with a foreclosure filing), South Carolina (one in every 1,982), Illinois (one in every 2,570), Delaware (on in every 2,710), and Nevada (one in ever 2,747).

Among metro areas with populations of a million or more, Tampa posted the highest foreclosure rate at one in every 1,373 housing units.

Following Tampa were Jacksonville (one in every 1,576 housing units), Orlando (one in every 1,703), Riverside (one in every 1,983), and Cleveland (one in every 2,114).

What a mess.

The good news is that it looks like there will soon be a lot of homes on the market in Florida.

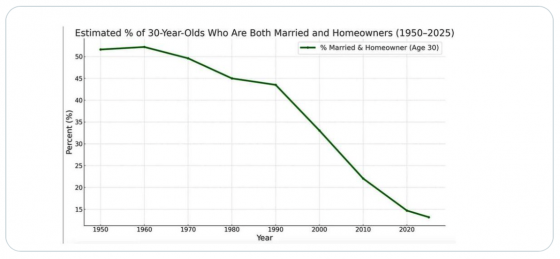

We live at a time when our nation is facing a very serious housing affordability crisis, and this has hit our young adults particularly hard.

The following chart which was once posted by Charlie Kirk demonstrates how home ownership among young adults has plunged in recent years…

These days, a lot of young adults are convinced that they will never be able to become homeowners.

Others that have really stretched themselves financially to purchase homes are now being hit with foreclosure notices.

I really detest what Wall Street has done to the housing market, and now we are reaping the consequences.

Renting is the primary alternative to home ownership, but renters are having a really hard time right now too.

As Daisy Luther has aptly pointed out, vast numbers of renters are being ruthlessly evicted from their homes in this very harsh economic environment…

Rents in America are ridiculously high in many areas, and nearly impossible to find in other areas. This is harder to track than foreclosures for two reasons.

Nobody official is keeping track of evictions, so we have to rely on extrapolated data from regions that do have somebody watching. One example of this is a company called “Eviction Lab” that tracks data from ten states, but only in specific cities and counties in those states. Even with this sparse reporting, their home page shows more than a million evictions over the last year, and more than 78,000 just last month.

The other reason we don’t have official numbers is something called “informal evictions.” Some states have laws against dramatic increases in rent, but not all states do. Both my daughter and I, living in a metro area, have faced a vast increase in rent when our leases were up. For my daughter, the increase was $900 a month and for me it was $600 a month.

Most of the country is just barely scraping by from month to month.

So it is really easy to push most Americans into a state of financial disaster.

Just look at what is happening with subprime auto loans.

The share of those loans that are at least 60 days delinquent has reached the highest level ever recorded…

The share of subprime borrowers at least 60 days behind on their auto loans rose to 6.65% in October, the highest level on record, according to Fitch Ratings data going back to the early 1990s.

As auto loan delinquencies spike, we are seeing a shocking surge in vehicle repossessions as well…

A near-record number of cars are being repossessed as Americans continue to fall behind on their auto loans amid mounting financial strain.

According to data from the Recovery Database Network (RDN), analyzed by CURepossession, 2025 has seen over 7.5 million repossession assignments—authorizations given to an agency to recover a vehicle on behalf of a lender. Based on historic trends, this figure is expected to reach a record 10.5 million by the end of the year.

Although recovery ratios have fallen in recent years—potentially lowering the number of actual repossessions—it is projected that over three million cars could be repossessed in 2025, a level only reached in 2009 during the Great Recession.

Do you remember the “subprime mortgage meltdown” that we witnessed in 2008 and 2009?

Well, this time around we have a “subprime auto loan meltdown”, and a couple of very large lenders have already gone belly up…

PrimaLend, which serves the “buy-here-pay-here” auto financing market — where dealers sell and directly finance vehicles for customers with poor or limited credit — filed for bankruptcy protection last month.

Tricolor, which sold cars and provided auto loans mostly to low-income Hispanic communities in the Southwestern United States, also filed for bankruptcy in September.

Unfortunately, a lot more Americans will be getting behind on their mortgages and their auto loans during the months ahead because a lot more Americans will be losing their jobs.

With each passing day, we learn of more mass layoffs.

Today, it is being reported that Verizon “is planning to cut 15,000 jobs”…

The optics look awful for Verizon Communications if the Wall Street Journal’s report is accurate: the carrier is preparing for its largest job cuts ever just days before millions of Americans hit the road for Thanksgiving.

WSJ says Verizon is planning to cut 15,000 jobs. If that figure is correct, Bloomberg’s latest data suggests this would be about 15% of its roughly 100,000-person workforce. WSJ notes this would be the largest workforce reduction on record for the carrier.

Does this mean that Verizon’s customer service is about to get even worse?

Of course it would be exceedingly difficult for it to get any worse than it is right now.

By the way, you may have noticed that stock prices are absolutely plummeting.

I think that we will see a lot more market volatility in the days ahead, because global events are going to get quite chaotic.

We are truly living in one of the most pivotal times in all of human history.

Sadly, the vast majority of the population still doesn’t understand what is happening to us, and that is very unfortunate.

Michael’s new book entitled “10 Prophetic Events That Are Coming Next” is available in paperback and for the Kindle on Amazon.com, and you can subscribe to his Substack newsletter at michaeltsnyder.substack.com.

{kind=link}

Markets ARE not plummeting. They’re at record highs.

Trillions in new factory jobs are moving into CONUS.

Unemployment is going down.

Interest rates slowly coming down.

Oil is ratcheting down, supply is up.

Nuke power will be developed.

This is not a bad mix.

I’ll bet that if you tell the locals that you live in that 2-year-old housing development nearby, they will nod knowingly. Then as they turn away they will mutter under their breath, “Blue state refugee”.

“By the way, you may have noticed that stock prices are absolutely plummeting.”

I have not noticed this to any extent. Some fluctuations, but still close to all-time highs. Are you referring to some specific market?

Difference is, in 2008 dim-0s had just taken over the house of reps after being out of power for 6 years of glorious economic growth. Every time they gain some power with a Republican in the WH, they and their P.R. branch the MSM talk the economy into a hole.

…interest rates for residential homes is too high…the cost of food especially beef is too high…the ‘free benefits’ are too expensive for taxpayers to keep giving to ‘people of color’…there are too many blood-sucking border-jumpers still in the US causing fraud and violence daily…too many Marxist-Progressive-Liberal-Democrats being elected to state and Federal positions of influence…the doors have been open to the Islamic Haters of America who now are turning the state of Texas into a Islamic Strong Hold…to much apathy and dis-concern from ‘white Conservative God-fearing Americans who would rather sit by and watch the USA go down in defeat and internal moral decay than to ‘FIGHT-FIGHT-FIGHT’…if we lose America it’s our own damn fault…

This time around is a little different from 2008 when interest rates were at an artificial low of 1%. Now interest rates are around 5%. What’s different is our major cities have been taken over by Socialist Democrats and their friends BLM and Antifa. Wealthy urbanites are fleeing to more tranquil areas and buying properties with cash. This has driven up housing prices putting pressure on lower income buyers to take out aggressive mortgages that wind up in foreclosure. Different but the end result may be the same.

While foreclosures may be up, we are coming off historically low foreclosures. The Oct 2025 data, while higher than 2024, is still only 16% of October 2007, which was just before the Recession (37k vs 224k), according to the AP on 11/29/2007; even in Oct 2008 it was higher, at nearly 280k. According to HousingWire in Dec 2019, there were ~50k US properties with foreclosure filings, “the lowest monthly volume since Black Knight began recording the metric in 2000…” So while it may be increasing currently, it is nowhere near where it was in 2007, and still near historic lows.

Gold has doubled in price over the last two yrs. The value of the gold didn’t change, rather the value of the dollar plunged. Not good.

Youre not correct for an important reason.

When 75% of the mortgages were 5% or lower, foreclosures were at a record low. No one loses a mortgage that cheap.

As more mortgages at 6% or higher enter the marketplce, the foreclosure rate is going to normalize. Ie before 2020

You need to compare foreclosure rates to 2020 and before, not 2024. Also, compare completion rates, not starts.

The correlation youre making doesnt apply until we see ctual foreclosures go higher than they were from 2016 to 2020, as a % of total mortgages.